Workshop held on 03 December 2015, Capital Hotel, Addis Ababa.

ESSP hosted its first workshop on insurance in Addis Ababa, along with partners – ILRI and BASIS. The program appointed contributions from different aspects of insurance, citing examples across Ethiopia. Over 50 people attended from donors, research communities, government and insurance businesses.

This is a relatively new area of business for Ethiopia, and which continues to generate a lot of discussion on how insurance can fit into the lives of rural communities; farmers simply need to know that if they have a loss, will they get paid. A variety of efforts introducing index insurance in Ethiopia have been implemented in the past few years. Several of these innovative projects are particularly promising, and deserve closer examination

During the workshop, Christopher Barrett from Cornell University described the Index-Based Livestock Insurance (IBLI), both from the research perspective and how to make the index suitable in practical terms. The index is based on average losses in a community and not for individual losses, the principle being that if gains fall below a certain threshold, payment is received. The key determinants for farmers are: price (based on how well the policy is designed) and education (to establish effective demand), along with liquidity (how much cash in hand a farmer has) and the size of herds (when dealing with livestock). Overall, Christopher Barrett expressed that the research shows that people are generally better off with IBLI coverage, significantly decreasing the likelihood of distress sales and missed meals. For further details see the presentation.

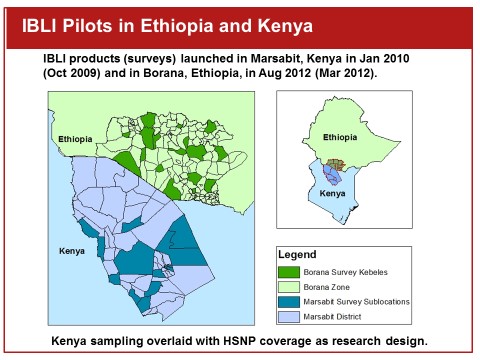

Figure 1 – IBLI Pilots in Ethiopia and Kenya

Insurance take up is generally disappointingly low. So tackling the barriers, such as index design, policy and institutional infrastructure, establishing effective demand, these all impact scaling up, as discussed by ILRI’s Andrew Mude. The difficulty arises when trying to develop indexes from often poor data. However, with the use of remote sensing techniques to help in an asset protection program and quality data, along with geographic and temporal coverage, pricing and fitting index to the risk, this moves towards creating a solution to move up to scale.

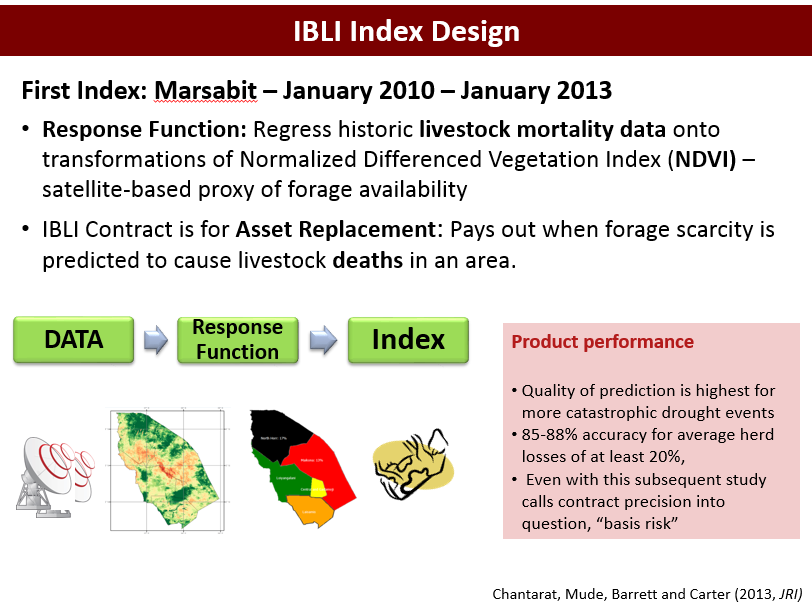

Figure 2 – slide from presentation

From a different perspective, Tesfaye Desta from Oromia Insurance described the challenges to increase purchases of insurance products, having implemented the pilot. He remained optimistic that in time, reaching out to customers will reap benefits. Solomon Zegeye from Nyala Insurance reflected on the involvement of Dashen Bank and other partners to help farmers finance the often high insurance premiums. He described EPIICA – an innovative project that aims to give insurance and credit to farmers. Many challenges are identified, but Zegeye clearly expressed a way forward focusing on building capacity, addressing regulatory issues, and working in collaboration and committing to succeed.

A number of speakers commented on the difficulty at getting banks or other private sector organizations involved in insurance in Ethiopia because of the risks involved. If this risk, or basis risk, is reduced so that the probability of farmers not being paid when they should have been paid is shrunk, this would go a long way to encourage farmers of the value of insurance to protect their assets.

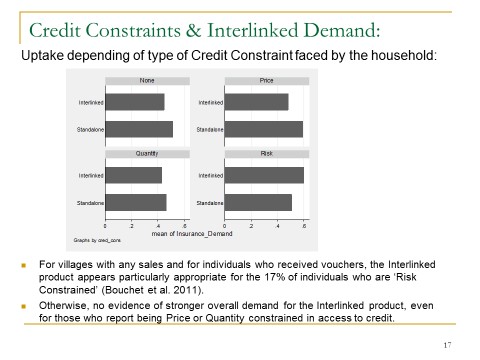

Another angle on index insurance was explored by Craig McIntosh form University of California on weather index insurance, where rainfall is used as the measure for creating the index. The research highlighted the importance of credit availability with insurance uptake, and notably, those kebeles covered by the PSNP, people were less willing to fund insurance themselves.

Figure 3 – Credit Constraints and Interlinked Demand

As pointed out by Michael Carter from the University of California, we know everything about risk, but what can index insurance do? Carter shared thoughts about some of the already mentioned challenges, but voiced the question “can we make a more stable situation for the poor by reducing vulnerability and incentive investments?” In his research, Carter used satellite information to help predict yields, but then followed this by testing the data on the ground through audits. One of the key factors in taking up insurance is trust, so demonstrating ground truth in this way was shown to give greater confidence to farmers. Bad data is often the reason for high premiums, so if this could be addressed, it would make a significant difference.

Weather-index insurance was investigated further from the perspective of informal (through “iddirs”) and formal insurance in the Ethiopian setting. Guush Berhane expressed that demand was disappointingly low for reasons largely resulting from basis risk, trust and high transaction costs. In research undertaken two years ago, the focus was to mitigate basis risk through “gap insurance” (see ESSP Outcome Note 04). There appears huge variation in interest across the country, however, the risk sharing element introduced through local community “iddirs” seems to instill trust that emergencies can be tackled more effectively. IFPRI worked with Buusaa Gonofaa – micro-finance institution – in this research as their coverage is across regions. Teshome Dayesso (CEO, Buusaa Gonofaa) described how they created policies that matched requirements. Although the pilot was successful in the uptake of insurance, those involved in the pilot considered how this could be successfully scaled up. In his final comments, Teshome Dayesso proposed the collaboration with cooperatives or with other partners as a means of going forward.

Figure 4: Poster to illustrate the gap insurance among farmers

Finally, the workshop touched on how agricultural insurance is coping in the face of increased climate instability. Lena Heron from USAID described that we are working towards the approach to improve the nimbleness of humanitarian responses, improvements to markets, and water and resource management in general. Heron expressed that some improvements in resilience were being observed, but El Niňo related droughts have been very difficult to absorb such shocks by such designs. Therefore, seeking to transfer the “shock” out of the system with insurance instruments that tackle resilience, is the challenge we face.

Michael Carter reviewed models that consider variables that influence people’s ability to manage their vulnerability, but then by adding climate change totally alters the picture. In his final session, Carter revisited integrating social protection and the government’s involvement to help keep any kind of insurance program in the reach of the most vulnerable, considering “risk pricing in the face of uncertainty” (see Carter’s presentation).

The final panel discussion generated many points and further questions. There is no conclusive answer on how to drive insurance uptake in Ethiopia. However, from the quality research, collaborative working with financial and legal systems, better understanding of the nature of risks farmers face, investing in data and other local infrastructures, improving local capabilities in designing insurance products, consumer education, building trust with the farmers, and improvements in regulations, are among those elements that will move the agricultural index insurance industry to scale and bring promise to many of the poor and risk-prone agricultural communities in Ethiopia.

To download any of the conference presentations, visit Slideshare.

Here are some of ESSP’s published works:

• The impact of research on weather index insurance (Outcome Note 04)

• Weather-based insurance for African farmers has issues (SciDevNet Article)

• Insuring against the weather (ESSP Research Note number 20)

• Saving for a Sunny Day (IFPRI Insights Magazine)

• Diagnostic Study of Providing Micro-Insurance Services to Low-Income Households in Ethiopia (ESSP-EDRI Report)

• Adoption of Weather Index Insurance. Learning from Willingness to Pay among a Panel of Households in Rural Ethiopia (ESSP Working Paper 27)

Visit our website for more information.